Advances in Pharmaceutical and Ethnomedicines

Mini–Review Article

Advances in Pharmaceutical and Ethnomedicines. 2 (2): 18 – 20Pharmaceutical Industry Challenges and Generic vs. Patent Brands, Global Perspective

Muhammad Irfan Akram

-

Pharmaceutical Marketer (Head of Sales and Marketing Agror Pharma Private Limited) Lead Consultant–Pakistan

*Corresponding author:irfanpharmacist@hotmail.com

ARTICLE CITATION:

Akram MI (2014). Pharmaceutical industry challenges and generic vs. patent brands, global perspective. Adv. Pharm. Ethnomed. 2 (2): 18 – 20.

Received: 2014–03–20, Revised: 2014–04–02, Accepted: 2014–04–03

The electronic version of this article is the complete one and can be found online at

(

http://dx.doi.org/10.14737/journal.ape/2014/2.2.18.20

)

which permits unrestricted use, distribution, and reproduction in any medium, provided the original work is properly cited

ABSTRACT

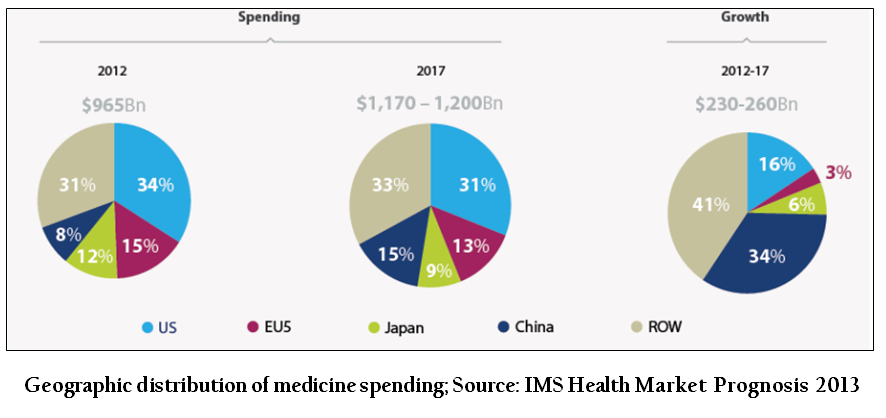

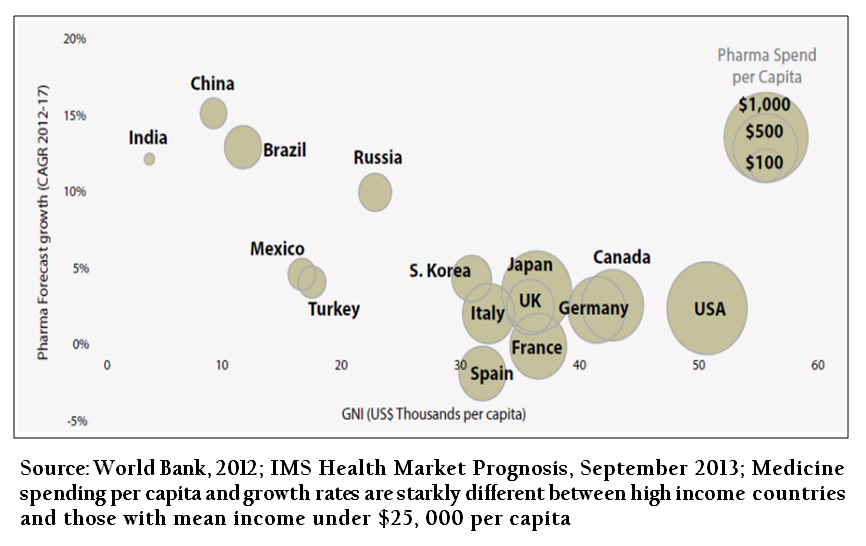

Pharmaceutical industry is the main pillar of Health Sector in terms of business volume. Global spending on medicines will exceeds 1 Trillion US$ in 2014 claimed by IMS health (Original name was “Intercontinental Marketing Services”)3. The US, EU5 (combine of Germany, France, Italy, UK & Spain), Japan and China will accounts for 67% of the total Global medicine spending. Total Global spending on Generics will increase from 27% in 2012 to 36% in 2017; however it accounts 63% in Pharmerging markets (China, India, and Israel etc)3. Developed markets of North America, Europe and Japan sees limited single digit growth–spending mainly due to economic health policies and measures taken by regulatory authorities to encourage the use of cheaper and economical medicines. Pharmerging markets showed double digit spending growth mainly due to increase in health coverage, economic growth and demographic changes. Uncertainty exists in developed markets to a greater extent. Use and access to innovative medicines is very restricted even in European countries most of the people have very limited access to these innovative medicines. Affordable Care Act. Imposed by US Govt. brings uncertainty as it enrolls many uninsured persons, to the speed of payment system changes and shift in the service delivery including negotiations between payers and service providers.

Two factors would be the major drivers of growth of pharmaceutical industry in coming years, increased spending on medicines in emerging markets and increased spending on new drugs for cancer and orphan diseases. Use of medicines is complex phenomenon and varies among geographic segments (developed countries vs. under–developed countries, regulatory authorities of individual countries, patent laws and Trade related intellectual proprietary rights–TRIPS) and demographic segments (age, sex, lifestyle and congeniality etc.).

Pharmaceutical industry on basis of products, can be divided into,

1. Research based drug molecules manufacturers

2. Generics medicines manufacturers – Low cost medicines

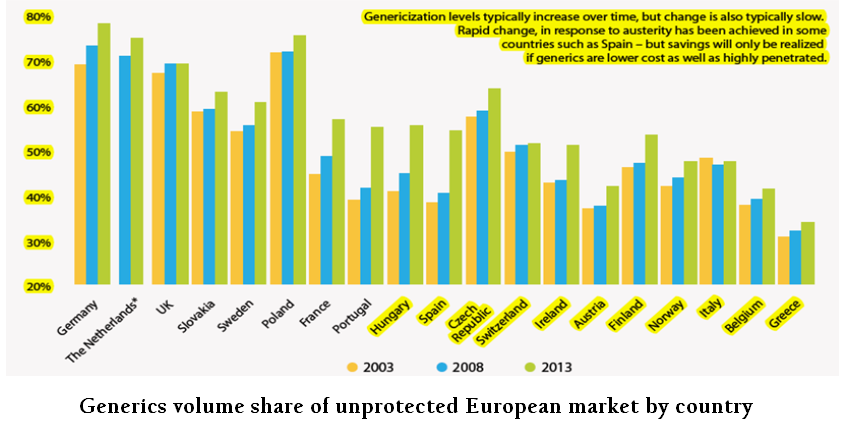

Companies spend millions of $ on Research & Development and later on only few molecules can reach to Phase 3 clinical trials and finally they get approval from regulatory authorities to market only one to two molecules those which have been found safe and effective in large human population. Mostly research medicines got respectable business across the World to surpass their original research cost within few years of market launch. If we see the whole phenomenon of a Research Brand from Development to Production (Formulation) to Distribution to Market, huge cost is involved. Usually companies spend large budgets on promotion of research brands to not only gain market share but also establish their brand loyalty to develop threats for low cost generics to enter into market. Pharmaceutical companies’ mergers and acquisitions in past 5 years were tremendous on the edge to curtail their expenses to meet the global economic recession and maintain their viability. Another reason of these mergers is due to dropping off patents of many blockbuster brands and increasing growth trend of ‘generic market’ that caused significant drop off revenues, so this is the only reason that most of the MNCs also entered into ‘generic medicines’ business. According to the Department of Commerce, there has been increased globalization in both brand name and generic drugs over the last two decades. India, China, and Israel do the most manufacturing of generics, and the fastest–growing pharmaceutical manufacturing centers are in South Korea, Brazil, the Middle East, Russia, and Southeast Asia. The Department of Commerce reports that Australia, France, Greece, Japan, and Switzerland have generic–drug utilization rates below 30%, in contrast to the U.S. rate of 86%2. Research suggests that foreign governments’ price controls have delayed the launch of drugs in different markets, thereby adversely affecting patients’ access to new medications. In 2013 and 2014, 14 and 18 drugs will come off patent, respectively; in 2015, only nine drugs will lose their patents. After 2015, very few breakthrough drugs will be coming off patent, so manufacturers of generic drugs will encounter a slower growth in revenue.

The German generics market had total revenues of $9.2bn in 2012, representing a compound annual growth rate (CAGR) of 0.8% between 2008 and 2012. The performance of the market is forecast to accelerate, with an anticipated CAGR of 2.7% for the five–year period 2012 – 2017, which is expected to drive the market to a value of $10.5bn by the end of 20171.

The mix of total global spending on medicines will shift toward generics over the next five years, rising from 27% to 36% of the total by 2017, even as brands will continue to account for more than two thirds of spending in developed markets.

The use of generics will be at its highest in pharmerging markets where 63% of the spending will go to generic products.

Absolute spending on brands in developed markets will decline by $113bn over the next five years due to losses of exclusivity, slower uptake of new medicines and more restrictive access approaches.

Traditional pharmaceuticals – typically used to treat chronic diseases in primary care – will increasingly be dispensed as generics and as a result total spending will only rise 5% by 2017 in developed countries.

Conversely, patients in pharmerging markets will increasingly have access to affordable generics for primary care treatments and total spending on traditional pharmaceuticals in these markets is expected to rise from $199Bn in 2012 to $336Bn in 20173.

Specialty medicines – used for conditions that require complex treatment and usually command higher prices –will be the biggest driver of branded drug spend growth and most apparent in developed markets where spending is expected to increase by 30% over the next five years.

Use of specialty medicines in pharmerging markets is at very low levels, but the costs areexpected to rise by nearly 90% between 2012 and 2017.